Bankaool, a regulated Mexican commercial bank, has worked toward operational and digital transformation since new leadership took over in 2023.

The institution has grown from roughly 300 employees to more than 1,800 and expanded its branch footprint nationally.

Moises Chaves, chairman of Bankaool, has been outspoken about Bankaool’s vision, which includes compliance as an organic part of growth and digital modernization that helps the bank better serve customers.

Driving the digital vision from the inside is Lucía Rodríguez, Bankaool’s Head of Innovation. Her approach to building financial products doesn’t start with technology. It starts with people:

- How they interact with money

- What they fear

- What they trust

- What makes them feel like a financial institution actually understands them

In an industry currently racing to deploy artificial intelligence, Rodríguez is asking a more fundamental question: If everyone is doing it, can you really call it innovation?

The Problem With Chasing Trends

Artificial intelligence adoption is strong in financial sectors, and for good reason. According to McKinsey, generative AI alone is likely to create $200-$340 billion in annual value by driving savings or revenue for the banking industry.

Consumer trust in AI has come a long way as well. According to CX Dive, more than 60% of customers are comfortable with some level of AI use behind the scenes of financial products. When asked specifically, users tended to support AI for fraud detection and tracking and calculation activities.

However, consumers don’t want AI operating in a vacuum that also includes their money. More than 80% want some human involvement, and less than 25% trust financial recommendations generated solely by AI.

Rodríguez has watched the industry’s AI race closely, and her skepticism isn’t about the technology itself. It’s about chasing trends. Today, she observes, it’s AI. A few years ago, it was blockchain. Before that, the dot-com boom.

Each wave brought new, possibly better, functionality. However, through every trend, banks that stayed focused on the people they were serving while carefully adopting what worked for them tended to be the lasting players.

For Rodríguez, that distinction shapes Bankaool’s approach to product development. Before her team asks what a product can do, they ask who it’s for, what friction they’re experiencing and what it would actually mean to remove it.

What People-First Design Looks Like

“Our goal is to integrate AI responsibly,” says Rodríguez. “That complements, but never replaces, the human side of banking. In the end, we’re still people who develop technology for other people.”

At Bankaool, that philosophy shows up in product and service decisions such as:

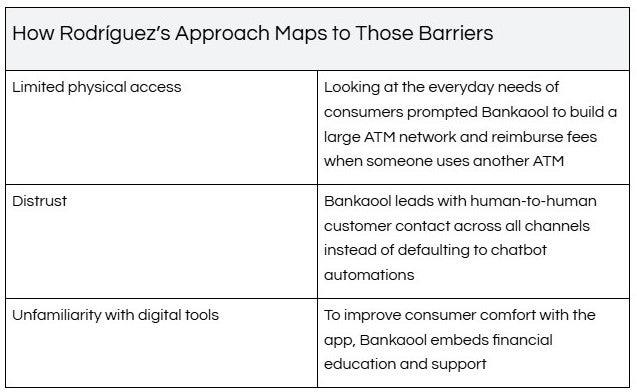

- Reimbursing fees when customers withdraw from any bank’s ATM because, as Rodríguez puts it, customers shouldn’t be charged to access their own money.

- Rejecting chatbots and automated call centers in favor of human-to-human customer contact across all channels

- Implementing AI-assisted business account opening to streamline document validation for corporate clients

- Developing financial health assistants that analyze user habits and offer personalized recommendations

- Launching an in-app investment simulator designed to “teach by doing”, helping users build financial literacy through their own account activity

Bringing the “Analog” to Digital

“We push ourselves to search the analog for memorable and endearing experiences we can bring into the digital space,” says Rodríguez.

Rather than implementing the latest technology to routinely bolster the bottom line, Rodríguez’s team starts with the human component. What drives a person to interact with a financial service in the first place? Nostalgia, need, trust, fear a sense of belonging? Where can technology connect with those drivers and offer genuine support?

The ATM network is a good example of that thinking in practice. The starting point was a human observation: sometimes people need cash. From there, the questions became:

- What friction stands between a customer and getting cash?

- What would it take to remove it?

The answer was to build Mexico’s largest ATM network and eliminate the fees that penalize customers for using them.

Rodríguez applies the same approach across her team’s work. The goal, as she frames it, is to understand people deeply enough that the technology almost becomes secondary.

What It Means for Financial Inclusion

At a time when around half of Mexican adults are unbanked, and more than 80% prefer to use and receive cash over other payment methods, Bankaool is using Rodríguez’s approach to meet consumers where they are:

- What friction stands between Mexican consumers and banking?

- What does it take to remove that friction?

The barriers are well documented:

- Limited physical access is a structural problem, as 87% of rural municipalities in Mexico lack an ATM entirely.

- Distrust of institutions runs deep, driven in part by concerns about hidden fees and fraud.

- For many potential customers, unfamiliarity with digital tools, combined with a longstanding preference for face-to-face interaction, makes digital-first banking feel inaccessible rather than convenient.

The Real Innovation Is Human

If everyone is racing to implement the same tech and AI, can you really call it innovation?

Rodríguez’s answer to her own question is that technology isn’t innovation in itself. It becomes innovation when it solves a real problem for a real person.

The innovations helping Bankaool grow don’t start with a technology decision. They start with an observation about how people live and what gets in their way.

In a sector where pressure to adopt the latest tools is constant, a disciplined people-first approach is harder to maintain than it sounds. For Bankaool, it’s become the organizing principle behind how the bank grows. And who it grows for.